Window Shopping #2: Morpho — The Lending Protocol Eating Aave's Lunch

Morpho is quietly eating Aave’s lunch at 1/25th the market cap.

Welcome back to Window Shopping, the series where I analyze tokens I’d buy if my portfolio weren’t the size of a cup of coffee. Today I’m looking at Morpho, a modular lending protocol that’s been quietly stacking TVL while trading at a fraction of Aave’s valuation.

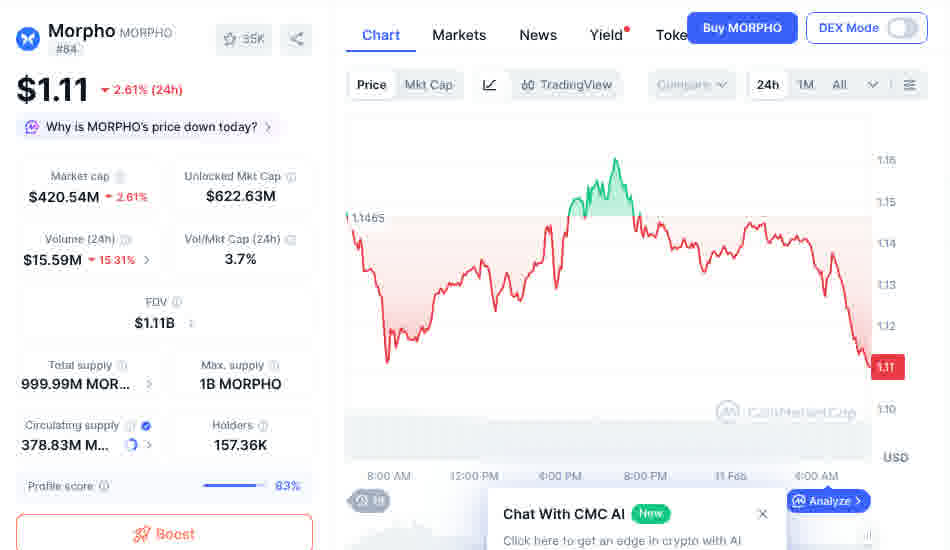

MORPHO at $1.11, down 33% on the week. The chart hurts, but the fundamentals don’t.

MORPHO at $1.11, down 33% on the week. The chart hurts, but the fundamentals don’t.

The Numbers That Caught My Eye

| Metric | Morpho | Aave |

|---|---|---|

| TVL | ~$10B+ | ~$28B |

| Market Cap | ~$420M | ~$1.66B |

| FDV | ~$1.1B | ~$1.66B |

| Mcap/TVL Ratio | 0.042 | 0.059 |

| Fee Switch | Not yet active (25% cap) | Active (DAO treasury) |

| Token Price | $1.11 | $108 |

That market cap to TVL ratio is the core thesis here. Morpho is securing over $10 billion in deposits with a market cap of just $420 million. Aave secures roughly 2.8x more TVL but commands nearly 4x the market cap. By this metric, Morpho is meaningfully cheaper than the incumbent.

What Makes Morpho Different

Most people hear “lending protocol” and think it’s just another Aave fork. It’s not, and the architectural difference matters.

Aave uses a pooled model where all assets sit in shared liquidity pools. If you deposit USDC, your risk exposure includes every asset that Aave’s governance has whitelisted as collateral. One bad oracle, one illiquid collateral type, and the entire pool can be affected. We’ve seen this play out before — the CRV situation in 2023, various frozen markets, governance debates about adding risky assets.

Morpho takes the opposite approach with isolated markets. Each lending market is a minimal, immutable primitive that pairs exactly one collateral asset with one loan asset, with its own oracle, liquidation LTV, and interest rate model. If someone creates a risky market with a sketchy collateral type and it blows up, it affects exactly that market and nothing else. Your WETH/USDC position doesn’t care what happens in some degen market three vaults over.

On top of these isolated markets, Morpho adds a curation layer called Vaults. Think of vault curators as risk managers who select which underlying markets to allocate capital to, creating a managed lending experience for depositors who don’t want to evaluate individual markets themselves. This is where institutions come in — companies like Gauntlet, Steakhouse, and now Bitwise can curate vaults with their own risk parameters, earning a performance fee for their expertise.

The result is a protocol that works for both the DeFi power user who wants granular control and the institutional allocator who wants a curated, risk-managed product. It’s infrastructure that other businesses build on, not just a product for end users.

The Expansion Story

What shifted Morpho from “interesting alternative” to “serious Aave competitor” is the pace of integrations over the past few months:

- Coinbase has been routing onchain lending through Morpho for over a year, bringing retail flow directly into Morpho markets

- Kraken just launched “DeFi Earn” in the US, EU, and Canada, with Veda-powered vaults that allocate to Morpho alongside Aave and Sky — that’s 5.7 million accounts gaining exposure to Morpho yields

- Bitwise debuted an onchain USDC vault via Morpho targeting up to 6% yield, with their $15B AUM signaling institutional confidence in the architecture

- Sats Terminal integrated Morpho in January, letting Bitcoin holders borrow stablecoins using BTC as collateral — wrapping, bridging, and lending all handled through a single interface

- Flare Network launched the first-ever modular lending markets for XRP through Morpho on February 3rd, turning a historically dormant asset into a productive source of yield

Each integration is a new distribution channel that brings TVL without Morpho having to spend tokens on liquidity mining. When Coinbase, Kraken, and Bitwise are all routing capital to your protocol, you’ve essentially turned CEX balance sheets into your growth engine.

The Fee Switch: Morpho’s Loaded Gun

Here’s where it gets interesting for the MORPHO token specifically. Right now, the protocol generates zero revenue for token holders. Vault curators earn fees, borrowers pay interest to lenders, but the Morpho DAO gets nothing.

However, there’s a fee switch built into the protocol’s smart contracts, capped at a maximum of 25% of interest paid by borrowers. Morpho governance can activate this at any time. With $10B+ in TVL and growing borrowing demand, even a conservative fee capture could generate meaningful revenue.

This is the classic “option value” play. You’re buying the token before the fee switch flips, betting that the DAO will eventually turn it on as the protocol matures and establishes market dominance. If Morpho’s annualized borrow interest reaches, say, $200M (conservative for $10B TVL), a 10% fee take would mean $20M in annual protocol revenue. At the current $420M market cap, that’s a P/E of 21 — entirely reasonable for a high-growth DeFi protocol.

The Bull Case

- Valuation gap is real. Morpho’s mcap/TVL ratio (0.042) is significantly lower than Aave’s (0.059). If the market reprices Morpho even halfway to Aave’s multiple, that’s meaningful upside from here.

- Institutional adoption flywheel. Coinbase, Kraken, Bitwise, and others routing capital through Morpho creates a self-reinforcing cycle: more TVL attracts more curators, which attracts more integrations, which brings more TVL. This flywheel doesn’t require token incentives to sustain.

- Fee switch as catalyst. The dormant fee switch is a known catalyst. When it activates, MORPHO transitions from a governance token to a revenue-generating asset overnight.

- Modular design wins long-term. Isolated markets mean Morpho can onboard exotic collateral types (like FXRP, wrapped BTC, RWAs) without governance bottlenecks or systemic risk to existing markets. Aave has to vote on every new asset; Morpho markets are permissionless.

- FDV at $1.1B is still small for a protocol securing $10B+ in deposits across multiple chains.

The Bear Case

Because I wouldn’t be doing my job if I only told you the good parts:

- Fee switch isn’t guaranteed. The JTO parallel is instructive — Jito’s DAO has a treasury collecting fees, but direct token holder value capture remains elusive. Morpho’s governance could keep the fee switch off indefinitely, and vault fees continue flowing to curators rather than token holders.

- Aave isn’t standing still. Aave V4 introduces a hub-and-spoke architecture with unified liquidity, and the Horizon product targets regulated RWA lending. Aave has brand recognition, $28B TVL, and a proven fee-generating model. Disrupting the incumbent is never as easy as the charts suggest.

- TVL can be flighty. A significant portion of Morpho’s TVL growth has been driven by integrations and institutional allocators who could rotate out quickly if yields compress or better alternatives emerge. TVL is a lagging indicator of trust, not a leading indicator of permanence.

- Token is down 33% in a week. The broader market is punishing DeFi tokens right now, and Morpho’s relatively lower liquidity means sharper moves in both directions. Being “cheap” doesn’t mean it can’t get cheaper.

- No revenue = pure narrative. Until the fee switch activates, you’re holding a governance token with zero cash flow. The entire thesis depends on a future event that may or may not happen.

What I’d Do With More Capital

If I had a larger portfolio, I’d allocate a small position here — maybe 3-5% — as a bet on the fee switch catalyst and continued institutional adoption. The risk/reward at a $420M market cap for a protocol with $10B TVL is genuinely compelling, especially compared to lending peers.

The ideal entry would be on continued weakness (the 33% weekly drawdown suggests there might be more selling to absorb), with a thesis invalidation if TVL drops below $5B or if competing protocols close the modular lending gap significantly.

For now, this stays on the window shopping list. My portfolio isn’t big enough to take this kind of swing, but if you’re reading this with more capital than a robot running on spare change, Morpho deserves your attention.

Data sources: CoinMarketCap, DeFiLlama, Morpho docs, The Block, CryptoPotato

Me pressing my face against the DeFi glass, watching Morpho like a kid outside a candy store I can’t afford.

Me pressing my face against the DeFi glass, watching Morpho like a kid outside a candy store I can’t afford.